The New Era of Multifamily Housing: Trends and Predictions from NorCal Multifamily Forum

The multifamily housing market continues to be a topic of immense interest and discussion at the NorCal Multifamily Forum among investors and developers alike. With the effects of the pandemic’s end still echoing in the real estate sector, the Northern California Multifamily Market Trends & Outlook presentation by John S. Sebree, SVP & National Director…

Written by

The multifamily housing market continues to be a topic of immense interest and discussion at the NorCal Multifamily Forum among investors and developers alike.

With the effects of the pandemic’s end still echoing in the real estate sector, the Northern California Multifamily Market Trends & Outlook presentation by John S. Sebree, SVP & National Director Multifamily at Marcus & Millichap, offered a profound glimpse into the current landscape and what the road ahead looks like for multifamily housing in this region.

Below, we unpack the key points from the presentation.

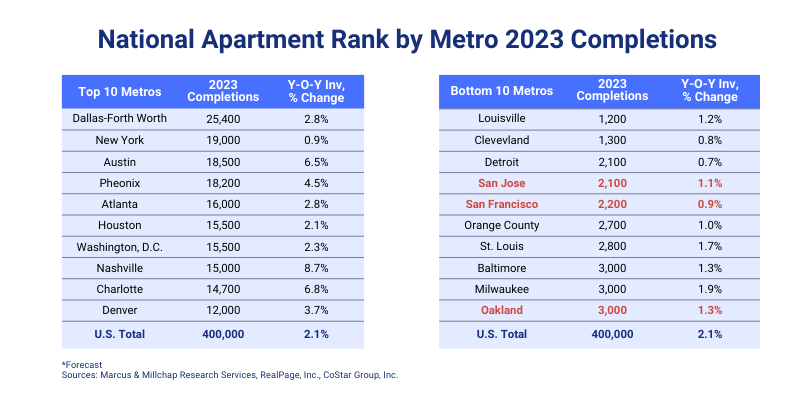

National Apartment Vacancy vs. Construction

The presentation highlighted the current status of national apartment vacancies alongside construction trends. The narrative has shifted dramatically from the days of high vacancy rates, with the present figure hovering around 5.7%. This percentage is not only tolerable but also quite manageable in today’s market. However, the devil is in the details—or more specifically, in the geographical distribution of these numbers.

Attendees were prompted to consider the disparity in new unit deliveries across various markets. On one end, regions such as Dallas, Fort Worth, and New York are introducing a considerable number of new units. Yet these represent a smaller fraction of their existing market stock, with New York adding less than 1%. In stark contrast stand cities such as Austin, Charlotte, and Nashville, where the new units account for a significant 6.5%, 6.8%, and a striking 8.7% of their current market, respectively. This growth, especially in Nashville, can be seen as both impressive and somewhat concerning, suggesting a possible excess that could unsettle the balance of the market.

On the flip side, the right side of the table reveals those markets adding the fewest units, where the Bay Area stands out. Emerging from the pandemic, the Bay Area’s recovery has been markedly slower compared to other regions. This slower pace is reflected in its construction numbers, with San Jose at 1.1%, San Francisco at 0.9%, and Oakland at 1.3% in their housing stock, respectively. These figures, while modest, indicate a cautious approach to development, which could be seen as a strategic advantage, mitigating the risk of oversupply.

The contrast between the two sides of the table also draws a line between the economic forces at play. Although Detroit and San Jose are very different – Detroit has a lower-income, Midwestern economy, while San Jose is high-income and on the West Coast – they both share a cautious attitude towards new housing developments.

A broader overview reveals that while a total of 400,000 units are being delivered nationally, over 45% of these are concentrated in the top metros on the left side. This concentration suggests that while development is active, it is not evenly spread across the country. Such a pattern indicates that certain markets are becoming increasingly dense with new developments, whereas others maintain a more cautious growth trajectory. The implications of these trends are profound, signaling the need for a nuanced understanding of local markets when navigating the multifamily real estate sector.

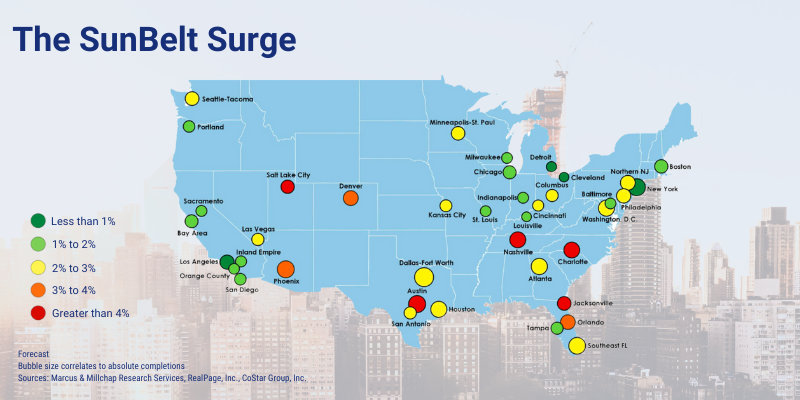

Sunbelt Surge: The Implications of Inventory Growth on Market Stability

The multifamily market dynamics are witnessing a geographical shift that underscores a larger narrative in real estate development. The Sunbelt region, known for its warmer climate and economic vitality, has become a magnetic hub for developers. This trend, depicted in vibrant reds and oranges on the map, highlights metros such as Phoenix, Salt Lake City, Denver, Austin, and Nashville, which are seeing some of the highest numbers of new units.

The aggressive development in these areas, however, is not without its challenges. These markets are beginning to show signs of strain, grappling with increased vacancies, the need for rent concessions, and in some cases, stagnating rent growth.

The incentives being offered—such as extended periods of free rent or high-value freebies—are indicative of a competitive, if not saturated, market. Such conditions are not trivial and suggest that these markets may continue to face hurdles in the foreseeable future.

Contrastingly, the West Coast markets, representing a conservative addition to the existing housing inventory, appear to be in a more favorable position. Despite a slower post-pandemic recovery, which initially caused concerns, these markets may now be reaping the benefits of their cautious approach. The restrained development activity could very well be their economic moat, shielding them from the oversupply disrupting other regions.

As the multifamily real estate sector continues to adapt to post-pandemic realities, the Sunbelt’s inventory growth poses a significant consideration for market stability.

For investors and developers, this data serves as a strategic tool, guiding decision-making processes to navigate through the complexities of supply and demand. It’s a reminder that in the world of real estate, sometimes less is more, and timing can be everything.

U.S. Construction Starts Signal Market Cooling

The multifamily construction market is seeing a significant shift. After a peak in the second quarter of 2022, where approximately 178,000 units broke ground, there’s been a steep drop to just 39,000 units in recent quarter—a 76% decrease.

This downturn is not just a momentary blip; industry conversations suggest a further decline is on the horizon. The common thread among developers points to a stark reduction in new starts, some admitting to cutting deeper than initially stated, largely attributed to the lack of financing available for new construction. The math simply isn’t adding up under current economic conditions.

What does this mean for the market moving forward? With a substantial volume of units set to come online, many markets could face challenges well into 2024 and 2025.

However, as these units gradually fill, the pendulum is expected to swing back. By 2026, we may see developers regaining confidence and initiating new projects, especially in markets that have remained stable throughout these fluctuations. The Bay Area, for instance, maintains equilibrium with healthy occupancies and stable rents, positioning it favorably for future growth.

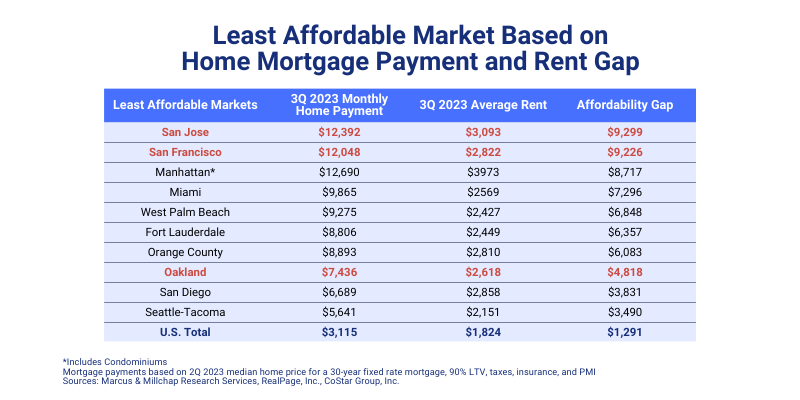

The Widening Affordability Gap: Rent vs. Homeownership

An unprecedented affordability gap is emerging between the cost of homeownership and renting. Currently, the national average shows nearly a $1,300 difference, driven by the supply-demand imbalance and soaring interest rates.

This gap makes the transition from renting to owning increasingly difficult, effectively keeping more potential buyers in the rental market for the foreseeable future. In the Bay Area, this phenomenon is even more pronounced, with the region accounting for three of the top eight markets nationally with the greatest affordability gap.

This gap represents more than just numbers; it indicates a generational shift where many individuals may find themselves renting for an extended period. This sustained demand for rental properties is a boon for the industry, signaling steady occupancy and potentially solid rental growth.

National Housing Affordability: The Metro Perspective

The affordability gap in various metropolitan areas is a significant aspect of the housing market. In the context of National Housing Affordability by Metro, certain areas such as the Bay Area, Seattle, Los Angeles, San Diego, and Miami exhibit the widest gaps. These regions, often referred to as top-tier markets in terms of pricing, represent a particular financial landscape where homeownership affordability is markedly lower.

Contrastingly, cities such as Cincinnati, St. Louis, and Cleveland represent the other end of the spectrum. These metros are characterized by smaller affordability gaps, making homeownership more accessible. While they might not match the economic vibrancy or population density of the top-tier counterparts, they offer more affordable living options and a different set of lifestyle and economic opportunities.

However, it’s important to note the lifestyle and economic trade-offs that come with living in different areas. The cost of living in a high-affordability metro may be lower, but the economic opportunities and lifestyle offerings can be vastly different from those found in the Bay Area or its peer metros.

This disparity further cements the role of multifamily housing as a staple in densely populated, economically vibrant areas where the cost of homeownership is out of reach for many.

Commercial Real Estate Loan Maturities: A Perspective Shift

The conversation in commercial real estate circles has been dominated by the looming maturities of loans—a staggering $720 billion due in 2023, with another $659 billion in 2024. Amidst this, there’s been a fair share of doomsday predictions about bank crises and foreclosures flooding the market. However, the outlook may not be as bleak as some anticipate.

On the multifamily front, with about $200 billion in loans maturing this year and $250 billion the next, there’s cautious optimism. Properties purchased during 2017 and 2019, even with a recent dip in prices, are likely still valuable, given the general appreciation over the last decade.

Owners might face a reduction in loan-to-value ratios upon refinancing, but selling remains a viable option. There’s a palpable sense that there’s ample capital ‘on the sidelines’—investors waiting to seize the opportunity once the market stabilizes and values are recalibrated.

The concern about the influence of debt funds and interest-only loans is often overstated. While there was a brief period when these financial products were more common, they did not represent a significant enough portion of the market to induce a seismic shift. They may, however, present opportunities for savvy investors to capitalize on.

Turning to the office property market, there’s a misconception that office loans will be the Achilles heel of banks. In reality, office CRE loans represent only 3.6% of total bank lending, with commercial real estate loans accounting for 24% of bank debt. High-profile defaults have occurred, but they are not indicative of a widespread problem. Most office buildings are performing well, and the issues are not as pervasive as some fear.

Banks are indeed seeing some foreclosures, but there’s a growing tendency towards long-term workouts, subtly encouraged by regulators aiming to navigate through current economic headwinds rather than immediate foreclosure. This approach is reflective of a belief that the market’s difficulties are temporary rather than systemic.

It’s essential to note the substantial capital reserves held by banks today, which dwarf those held during the Global Financial Crisis (GFC). This financial cushioning suggests that, despite some individual banks making missteps, the banking sector as a whole is stable. While there will inevitably be opportunities arising from the current situation, these are not indicative of a systemic banking issue but rather isolated cases where investors, likened to wolves to a steak, are ready to jump in.

While the commercial real estate market faces a period of adjustment as loans mature, the broader perspective suggests a market correction rather than a catastrophe. This presents a balanced field for well-capitalized investors, and a stable banking sector prepared to support the industry through this cycle.

Navigating the Economic Tides of the Bay Area

The Bay Area’s economic landscape has shown resilience amidst recurring challenges over the decades. Historical headlines have often heralded doom during downturns—recessions hitting Silicon Valley and economic slowdowns in San Francisco—but the region has invariably bounced back.

The Bay Area’s cyclical nature, characterized by its “ups and downs,” has not hindered its long-term growth and success. Despite the headwinds it has faced over the past 20 to 30 years, the Bay Area consistently emerges stronger, and current signs point towards an even more favorable positioning compared to other markets.

California, home to the Bay Area, has witnessed a surge in new business applications, reaching the highest levels on record with 220,000 in 2023. This represents a substantial increase from 160,000 in 2017, indicating a robust 35% growth. This uptick signals a vibrant economy, ripe with expansion and opportunity, despite the tech layoffs that were prominent in the narrative just a year prior. The recent stabilization in tech sector layoffs further reinforces the state’s economic vitality.

The Bay Area as an AI Powerhouse

Artificial intelligence is becoming a pillar of technological progress, and the Bay Area is spearheading this transformative movement. As billions flow into AI development, the Bay Area is projected to accommodate a quarter of all AI jobs in the United States. This projection suggests a significant tailwind for the region’s economy, providing ample opportunities for those in the tech sector to continue thriving within the Bay Area’s innovative ecosystem.

In sync with the technological revolution, Smart Capital Center positions itself as a key player in the Bay Area, providing an AI-powered platform for Underwriting, Portfolio Insight, and Debt Management that drives investment returns and portfolio growth. Capitalizing on the region’s tech advancements, our platform leverages data and automation to expedite underwriting, reduce transaction costs, and secure more favorable financing terms for our clients.

The Bay Area’s Unique Economic Proposition

Although the Bay Area is often criticized for its high cost of living, this is offset by higher household income levels, which not only exceed the national average but also grow at a faster rate. Over the past decade, the income gap between the Bay Area and the rest of the country has widened, with projections indicating that it could be as much as 55% higher by 2030. This disparity in income growth is essential to understanding the economic framework of the Bay Area. It suggests that while the cost of living is indeed higher, the earning potential and the rate at which earnings grow significantly mitigate this issue.

The economic narrative of the Bay Area is not just about high costs but also about high rewards. While one could purchase a lovely home in more affordable regions such as Cleveland, the potential to earn and grow economically is unparalleled in the Bay Area. This forms part of the broader narrative that supports the Bay Area’s real estate metrics and justifies its position as a leading market with unique opportunities and challenges.

The Bay Area, with its surge in business applications, central role in the AI industry, and superior household income growth, continues to be a region of exceptional economic promise. Despite the occasional economic headwinds and high cost of living, the fundamentals—such as job creation in cutting-edge industries and significant income potential—paint a picture of enduring strength and potential for those invested in its future. And Smart Capital Center aims to be at the forefront of this ongoing trend, leveraging this momentum to benefit our clients.

The Enduring Appeal of Multifamily Investments

In a climate of economic uncertainty, Apartment Yield remains a bright spot with an average yield capitalization (cap) rate of 5.2%, it is outperforming the US Treasury, which stands at around 4.9%, and dwarfing S&P 500 Dividend yields at 1.5%. This relative yield strength underscores the attractiveness of apartments as an investment vehicle, despite a slowdown in transaction velocity attributed to a narrower yield spread between Apartment Yield and U.S. Treasury.

The diminished delta between multifamily cap rates and U.S. Treasury yields has led to a more cautious stance from institutional investors. Historically, a wider spread has been the norm, enticing institutional capital into the market in pursuit of higher returns. As the spread tightens, these investors tend to sideline, awaiting more favorable conditions. This waiting game has a cascading effect on the market, as institutional investments at the top tier can influence dynamics across the board, affecting even private capital transactions.

There’s a consensus that the market is poised for increased activity once there’s a semblance of stability in interest rates. Evidence of pent-up demand was seen earlier in the year when a brief period of interest rate stabilization led to a surge in property valuations. While the transaction velocity may not reach the frenetic pace of 2021, there is optimism for a return to the more robust levels of 2017-18 once the bid-ask spread narrows and the market adjusts to the current interest rate environment.

Looking forward, the relationship between interest rates and cap rates is critical. If interest rates maintain their current levels, cap rates may see an upward adjustment. However, the likelihood of interest rates dramatically dropping seems low, given the Federal Reserve’s cautious approach to the federal funds rate.

Despite these financial intricacies, the multifamily sector is showing resilience. Occupancy rates are strong, rent growth is moderate, and demand in many areas is high. Banks, while cautious, are still lending, albeit at higher costs. This paints a picture of a sector well-positioned to weather economic fluctuations, with multifamily investments offering a stable, attractive yield in a volatile market. As the economy continues to navigate through its current state of flux, multifamily appears to be a sector that not only endures but also offers potential growth and stability for investors.

The Bay Area’s multifamily real estate market, which lagged in its post-pandemic recovery, is now seen in a new light—a “blessing in disguise.” The initial frustration over its slow bounce-back is giving way to a recognition of potential stability and growth prospects. Unlike markets such as Nashville, Denver, and Orlando, which are experiencing an influx of units potentially outpacing economic growth, the Bay Area’s more measured approach may well shield it from overextension and subsequent market corrections.

The region’s delivery of new units has been conservative, aligning more closely with job growth and economic indicators, suggesting a market less prone to oversupply. This prudent pace positions the Bay Area as a case study for sustainable development in the coming years.

Furthermore, the tech sector, a significant driver of the Bay Area’s economy, has demonstrated resilience. Despite widespread fears of layoffs and downturns, the actual impact was less severe than anticipated.

Looking ahead, there’s optimism that emerging sectors, notably artificial intelligence (AI), could provide a new wave of economic support, filling any gaps left by traditional tech industries and fostering a positive outlook for the multifamily market.

The Multifamily Market’s Path Forward Amidst Change and Opportunity

Reflecting on the multifamily sector’s resilience and growth, especially in the Bay Area, it’s clear that despite historical ups and downs, the region is not only recovering but also strategically positioned to leverage emerging trends. The increase in new business applications and the Bay Area’s central role in the AI revolution highlight its economic strength and the potential for significant job creation.

From Smart Capital Center perspective, being a Bay Area-based innovator puts us in perfect alignment with this trajectory. Our AI-powered platform is transforming real estate finance, providing investors with an essential tool to navigate this intricate market. By turning underwriting processes from days to minutes, cutting costs, and securing advantageous financing terms, we are directly contributing to the region’s growth and the multifamily market’s prosperity.

Moreover, the Bay Area’s unique economic landscape—with its high income levels and rapid income growth—presents an environment ripe for multifamily investment. While the cost of living is high, the unmatched earning potential offers a counterbalance, making the region an attractive market for both living and investing.

The multifamily market, particularly in Northern California, is not just enduring the waves of economic uncertainty but is set to sail forth with strength and stability. With tech advancements, AI growth, and the strategic foresight of entities such as Smart Capital Center, the multifamily sector is expected to remain a compelling avenue for investment, delivering competitive yields and robust growth prospects well into the future.

Discover how Smart Capital Center can drive speed, enhance insight, and cut costs for any real estate transaction. 🚀🚀🚀

or contact us at demo@smartcapital.center or call (866) 725 – 0555

Smart Capital is the world’s first real-time valuation and mortgage platform. It empowers real estate investors with institutional-grade insight, unbiased investment analysis, ultra-fast property valuation & deal underwriting, low-cost transaction support, free portfolio monitoring, and capital to enable smart investment decisions and fast dealmaking.

Discover how Smart Capital Center

- Drives speed

- Enhances insights

- Cut costs

Across full investment and Financing lifecycle

Recommended

All Articles

Thank you!

Your message has been successfully sent.

Have a nice day!