Emerging Trends and Strategic Insights from MBA CREF 24

The MBA CREF 24 conference in San Diego emerges as a cornerstone event for the commercial and multifamily finance industry, attracting top professionals to discuss trends, regulatory shifts, and innovative strategies. Below are some of the trends and takeaways from MBACREF24 that this article will cover: Driving Affordability and Safety in Housing The conference brought…

Written by

The MBA CREF 24 conference in San Diego emerges as a cornerstone event for the commercial and multifamily finance industry, attracting top professionals to discuss trends, regulatory shifts, and innovative strategies.

Below are some of the trends and takeaways from MBACREF24 that this article will cover:

- Driving Affordability and Safety in Housing: Prioritizing Workforce Initiatives and Tenant Protections

- $929 Billion in Commercial Mortgages Nearing Maturity

- CPI Surge Driven by Shelter Costs Signals Shift in Real Estate Market Dynamics

- Investment Expectations Shift with Rising Inflation and the Repercussions for Real Estate Financing

- Transforming Mortgage Transactions in a Volatile Market with AI-Powered Solutions

Driving Affordability and Safety in Housing

The conference brought to light several key issues, including the importance of workforce housing, tenant protections, and the challenges surrounding property conditions and insurance.

Kevin Palmer, Senior Vice President, and Head of Multifamily at Freddie Mac, emphasized the significance of workforce housing, stating, “This is where sponsors agreed to set aside a certain portion of their units, and keep them affordable for a period of time…basically for the whole duration of that loan. And by doing so we kind of lean in from a pricing and credit perspective, and it really helps to support the liquidity in that important space.” highlighting the commitment to affordability through the Workforce Housing Preservation Program.

Michele Evans, Executive Vice President and Head of Multifamily at Fannie Mae Multifamily, introduced a novel approach to workforce housing, the Sponsor-Dedicated Workforce product, designed to simplify industry compliance by focusing on rent restrictions over income limitations, thereby enhancing accessibility to affordable housing.

The discussion also touched on tenant protections, with Palmer noting the importance of creating “good decent safe housing, that families can be proud of and that helps to advance them individually and economically.” He underscored the value of community-building efforts and the need for further data collection on tenant notification protections to enhance tenant welfare.

Addressing property conditions, Palmer mentioned that feedback collected by Freddie Mac in 2023 led to policy adjustments aimed at improving property safety and condition surveillance. Evans also highlighted Fannie Mae’s efforts to ensure property conditions are managed appropriately, signaling a collective industry commitment to tenant safety and wellbeing.

The property insurance dialogue highlighted the necessity for adequate coverage in financing deals, with both Freddie Mac and Fannie Mae making case-by-case adjustments to accommodate the current market’s challenges. Evans optimistically noted, “Whenever you see challenges like this, I think there’s a great opportunity for the entire industry to get together, and really kind of take a look at it and see what we have, and what we can do, and how we can think about it,” pointing towards collaborative efforts to address and overcome these hurdles.

$929 Billion in Commercial Mortgages Nearing Maturity

During the conference, it was also shared that there is an impending maturity of a substantial portion of commercial mortgages.

In 2024, an estimated 20% of the $4.7 trillion in outstanding commercial mortgages, amounting to $929 billion, is poised to mature. This represents a notable 28% increase from the $729 billion that matured in 2023, signaling a critical time for lenders, investors, and stakeholders within the industry.

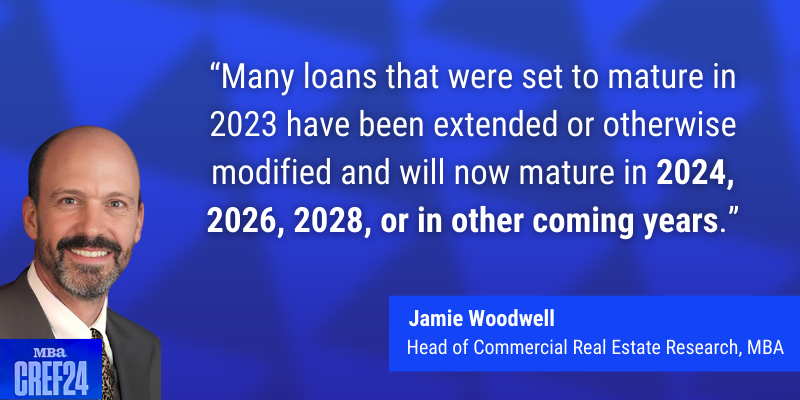

Jamie Woodwell, Head of Commercial Real Estate Research at MBA, sheds light on the dynamic at play, attributing the significant uptick in maturing debt to the prior year’s subdued transaction activity, alongside lenders’ and servicers’ adaptive measures such as loan extensions or modifications.

“The lack of transaction and other activity last year, coupled with built-in extension options and lender and servicer flexibility, has meant that many loans that were set to mature in 2023 have been extended or otherwise modified and will now mature in 2024, 2026, 2028, or in other coming years,” Woodwell explains.

Woodwell further explained that despite commercial mortgages’ inherent long-term nature, the current landscape is filled with challenges, including market volatility, interest rate uncertainties, and evolving property fundamentals.

Yet, this surge in maturities, combined with uncertainty around interest rates, a lack of clarity on property values, and questions about some property fundamentals have suppressed sales and financing transactions.

The maturity outlook varies considerably across different segments of the market. Notably, a mere 3% ($28 billion) of the multifamily and healthcare mortgages held or guaranteed by Fannie Mae, Freddie Mac, FHA, and Ginnie Mae are set to mature in 2024.

In contrast, depositories will witness 25% ($441 billion) of their mortgage balances maturing, with CMBS, CLOs, or other ABS seeing 31% ($234 billion), and credit companies, among others, facing a 36% ($168 billion) maturity rate.

The distribution of maturing loans also significantly differs by property type. While 12% of multifamily property mortgages are expected to mature in 2024, the figures rise to 17% for retail, 18% for healthcare, 25% for office properties, 27% for industrial loans, and a stark 38% for hotel/motel loans.

The reported figures represent the outstanding principal balances as of December 31, 2023. It is customary for most loans to reduce their principal over time, so it is expected that the balances upon maturity will be less than the amounts currently stated.

CRE Experts Share Key CRE Trends and Strategies

The closing super session served as a culminating event that gave participants rich discussions, insights, and forecasts shared throughout the conference.

This session brought together leading figures such as Maggie Burke from Capital One Commercial Real Estate, Victor Calanog from Manulife Real Estate Finance Group, Kevin Fagan from Moody’s Analytics CRE, Adam Fox from Fitch Ratings, and Jan Sternin from Berkadia, offering a comprehensive roundup of the week’s learnings.

Their collective expertise underscored the importance of industry advocacy, innovation, and the development of strategic foresight in navigating the ever-evolving landscape of commercial real estate.

CPI Surge Driven by Shelter Costs: Latest Numbers Not as Dire as Market Thinks

It is important to note that the cost of apartment rentals is a significant factor causing shelter inflation to appear much higher than it truly is. This is partly due to the expiration of discounts and concessions that were previously widespread, leading to an apparent rise in inflation.

This spike in inflation is expected to be short-term, as these concessions expire and the growth trend is unlikely to continue for years.

Consequently, the government may not raise interest rates as aggressively and might even consider lowering them. Although the overall CPI has increased, the government may treat the shelter inflation component as just one aspect of the broader inflation landscape, potentially softening the negative impact it could have on monetary policy decisions.

Investment Expectations Shift with Rising Inflation

Inflation was another part of the discussion, with the panel exploring its multifaceted impact on the commercial real estate sector.

One of the panel speakers emphasized, “Inflation isn’t just a number. It’s a force that reshapes investment landscapes, and for commercial real estate, it means recalibrating expectations.”

- The Impact of Interest Rate Hikes on Real Estate Development

In the panel’s dialogue, it was expressed that escalating interest rates are complicating the financial structuring of real estate transactions. “The surge in rates is making numerous deals challenging to justify, particularly those involving value-add strategies in equity investment scenarios,” one of the speakers explained.

“Overall, we’re experiencing delays across the board due to increased costs in financing and construction, leading to more time-intensive preparations for specific deals. Currently, we’re navigating a landscape of increased costs across the board, from financing to construction, which requires more time to align the products with specific deal parameters,” a panelist added.

“Critical decisions often hinge on forecasting where the 10-year Treasury will land, influencing whether we proceed or decline substantial investment opportunities, particularly when the math on building costs doesn’t add up. When you factor in the compounded effects of insurance and other expenses, the complexity intensifies. If interest rates remain elevated over an extended period, despite occasional dips, our strategies and deal structures must adapt accordingly.”

- CPI Inflation and Rent Trends: Expectations Versus Reality in Real Estate

The observed lag between asking rents and CPI shelter inflation, historically consistent, indicates a forthcoming alignment in market conditions and inflation figures, particularly noticeable in the multifamily sector. Despite expectations for a softening in the CPI shelter index, recent data revealed less movement than anticipated, partly due to nuanced lease terms emerging post-pandemic, adding uncertainty to when market rates and CPI shelter inflation will synchronize.

This situation underlines the complexity of interpreting economic implications within the real estate sector. The Federal Reserve, recognizing these dynamics, expects the overall inflation rate to gradually align with its 2% target, signaling an anticipated adjustment in market conditions and inflation measurements in the near future.

- Inflation Proofing Portfolios with Smart Real Estate Choices

The conversation also delved into the influence of inflation on asset valuation, highlighting that real estate could act as a hedge against inflation.

In an inflationary climate, the tangible value proposition offered by real estate assets becomes increasingly apparent. The strategic selection and management of these assets are crucial, exposing the need for investors to carefully consider their portfolio composition and management approaches to maximize returns and mitigate risks associated with inflation.

- The Ripple Effects of Geopolitical Issues on Global Trade and Supply Chains

A key topic addressed during the panel was the impact of geopolitical tensions on supply chains. One panelist expressed that the root of their most significant concern lies in geopolitical issues that have already exerted considerable pressure on global supply chains. “Why have we experienced such rampant inflation over the last few years?” they posed, attributing it to a multitude of factors, with supply chain disruptions being a principal component. The panelist highlighted that there has been a staggering increase, over 100% in some instances, in shipping costs due to these disruptions in the past three to six months.

Such concerns are not just hypothetical risks but real challenges that can lead to severe repercussions like a supply chain breakdown or an oil price surge. These potential events are distressing as they could force the Federal Reserve to reassess their strategy. “The supply side of the equation has changed,” they noted, acknowledging that while the demand side is gradually softening, evidenced by consumer behavior and an uptick in delinquencies, it’s the supply side that remains unpredictable and volatile.

The speaker voiced an unease about the unpredictability of geopolitical events, such as the initiation of conflicts or blockades in critical regions like the Red Sea, that could severely disrupt supply chains. These events are beyond the control of any single entity and have the power to significantly impact global economic stability and operations.

Experts Predict a Near-term Decrease in Interest Rates

There was a consensus among the experts on the anticipation of interest rates decreasing soon. This expectation is based on a blend of current economic indicators and market trends.

The panelists emphasized the significance of keeping a close watch on these developments, as any changes in interest rates could profoundly impact the commercial real estate market. This includes influencing borrowing costs, investment returns, and the overall dynamics of the market.

Federal Reserve Targets Employment and Price Stability for Economic Health

The speakers elaborated that the primary objectives of the Feds are to achieve full employment and to maintain price stability. These objectives guide the Fed’s careful monitoring of the unemployment rate and inflation metrics, such as the Personal Consumption Expenditures index.

The speaker outlined that, in their view, the Federal Reserve would be comfortable with interest rate adjustments when certain economic conditions are met.

For example, they suggested that a PCE number at or below 2.5%, coupled with an unemployment rate that creeps up to the 4-5% range, could signal a need for the Fed to lower rates. This is in consideration of current statistics, where the unemployment rate remains robust at 3.7%. Should it start to rise, the Fed might be compelled to act, potentially leaning towards a stance of non-intervention if the economy continues to perform well.

The speakers implied that they are watching two key figures: the PCE index and employment rates. A PCE that dips below 2.5% might offer the Fed more leeway to lower rates, potentially in June rather than March, and they would also consider labor market trends as an indicator for action. This nuanced take offers insight into the complex decision-making processes at the Federal Reserve, emphasizing the importance of a range of economic indicators in shaping monetary policy.

Rising Construction Costs Add Complexity to Real Estate Development

The panel addressed a critical issue that continually challenges the real estate development sector: the rise of construction costs. An observation by a construction expert set the stage, illustrating that since 1955, construction costs have only known one direction — upward. This assertion underscores a trend that could impact the feasibility of future development projects.

As the conversation progressed, a panelist echoed a widespread sentiment, “Everybody’s hoping that construction costs will eventually become more reasonable.” Yet, they were quick to temper this hope with the reality of historical trends which have shown a consistent rise, rarely offering any respite. This trend, combined with increasing insurance rates, creates a formidable barrier to financial viability for many projects, especially those relying on debt financing.

Discussing the ripple effects of these high costs, the panelist shared a personal account of the intricate calculations involved in development decisions, particularly how projections of the 10-year Treasury yield can influence the go-ahead of significant investments.

The dialogue then touched upon the future of interest rates. While slight fluctuations, such as a dip seen earlier in the year, offer a glimmer of hope, the ability to predict where the 10-year Treasury yield will land remains a complex task. The speaker reminisced about the difficulty of economic forecasting, referencing a Federal Reserve survey of economists’ past predictions compared to actual outcomes and the rare occasion when predictions aligned with reality in 2022.

A closer look at long-term interest rate trends revealed that despite the upheaval of recent years, the increase in the 10-year Treasury average has been minimal. Reflecting on a period of extraordinarily low rates, the speaker shared, “It feels almost unbelievable.”

The panel concluded with a reflective thought: “Rates only began rising about seven quarters ago, after nearly four years sub-two percent. Maybe we’ve just been spoiled all this time.” This comment hints at a potential recalibration of expectations within the market.

Adapting Real Estate Strategies with Creative Capital Solutions

In the context of the evolving commercial real estate landscape, particularly concerning affordable housing, the complexity of lending has increased significantly from what used to be a relatively straightforward process.

The panelists shed light on the intricate nature of current lending practices,

These creative capital solutions, offer a broad array of financing mechanisms designed to meet the unique challenges faced by today’s developers and investors. They often involve leveraging diverse funding sources, utilizing government incentives, and crafting innovative financial structures to achieve viability for projects.

Here are some creative capital solutions to consider:

- Public-Private Partnerships (PPPs): These partnerships distribute financial risk and rewards between public entities and private investors, facilitating projects that may not be viable through traditional financing.

- Low-Income Housing Tax Credits (LIHTC): These tax credits are a cornerstone for funding affordable housing, providing equity that incentivizes development.

- Green Bonds: Issued for environmentally sustainable projects, these bonds attract socially responsible investors and fund green initiatives.

- Crowdfunding Platforms: These platforms enable the pooling of resources from a wide base of investors, democratizing investment in larger projects.

- Flexible Loan Structures: Lending terms that are adaptable to project needs and timelines, allowing for more tailored financing solutions.

- Opportunity Zone Funds: Investments in designated areas that offer tax advantages to spur economic growth and development.

- Mezzanine Financing: This type of financing fills the gap between debt and equity, often used to secure additional capital that may not be available through traditional loans.

- Joint Ventures: Collaborations that leverage the strengths and resources of multiple parties to share risks and rewards.

- Land Leases: Reducing upfront land costs by leasing rather than purchasing, which can free up capital for construction and other critical project components.

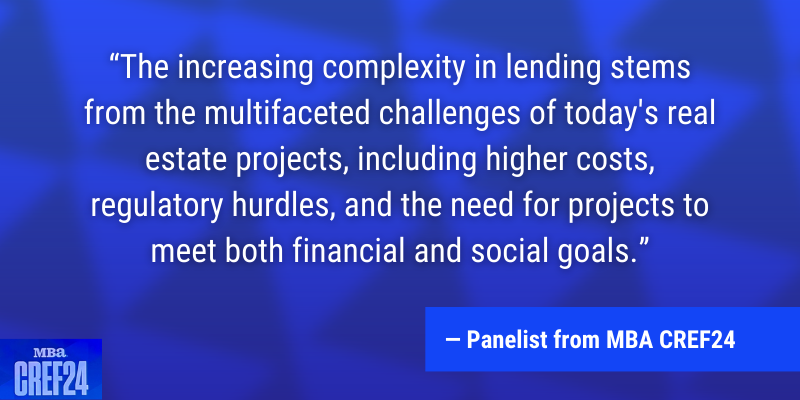

Panelists emphasized that the increasing complexity in lending stems from the multifaceted challenges of today’s real estate projects, including higher costs, regulatory hurdles, and the need for projects to meet both financial and social goals. The shift towards these creative capital solutions is a response to these challenges, requiring lenders and investors to think outside the traditional paradigms of real estate financing.

Smart Capital Center: Transforming Mortgage Transactions in a Volatile Market

The dynamic discourse from the recent conference underscores the rapid evolution of the commercial real estate finance sector, driven by fluctuations in loan maturities, inflation volatility, interest rates, as well as operational and construction costs. To align with these shifts, Smart Capital Center emerges as an indispensable ally in the industry, offering a powerful suite of tools driving operational efficiencies and better insight at every step of a mortgage transaction—from the initial stages of loan origination through asset management.

Wrap Up

The MBA CREF 2024 illuminated the dynamic shifts and emerging challenges within the commercial real estate finance sector, driven by the interplay of economic, technological, and political forces. Key takeaways underscore the pressing need for innovation in financing and asset management strategies – from developing new creative financing structures to leveraging technology to drive speed and efficiency, highlighting the transformative potential of automation and AI in reshaping the industry landscape.

Smart Capital Center stands at the forefront of these changes, leveraging its industry-leading technology, it empowers its clients to make data-driven decisions, optimize investment strategies, and achieve operational efficiency.

Explore the possibilities with Smart Capital Center further. Whether you seek consultation on navigating market challenges or wish to discover the capabilities of our AI-powered platform, our team is ready to demonstrate how we can support your goals. Book a demo today.

Discover how Smart Capital Center

- Drives speed

- Enhances insights

- Cut costs

Across full investment and Financing lifecycle

Recommended

All Articles

Thank you!

Your message has been successfully sent.

Have a nice day!